![SRA ‘Tax Adviser’ Checklist – Use this to see if your law firm’s practice areas are caught [AML]](https://www.jonathonbray.com/wp-content/uploads/bfi_thumb/dummy-transparent-obadi0wivgww4ihdae9xs8qbf69cenia3a5vcdxo0e.png "SRA ‘Tax Adviser’ Checklist – Use this to see if your law firm’s practice areas are caught [AML]")

What’s the SRA ‘tax adviser’ issue?

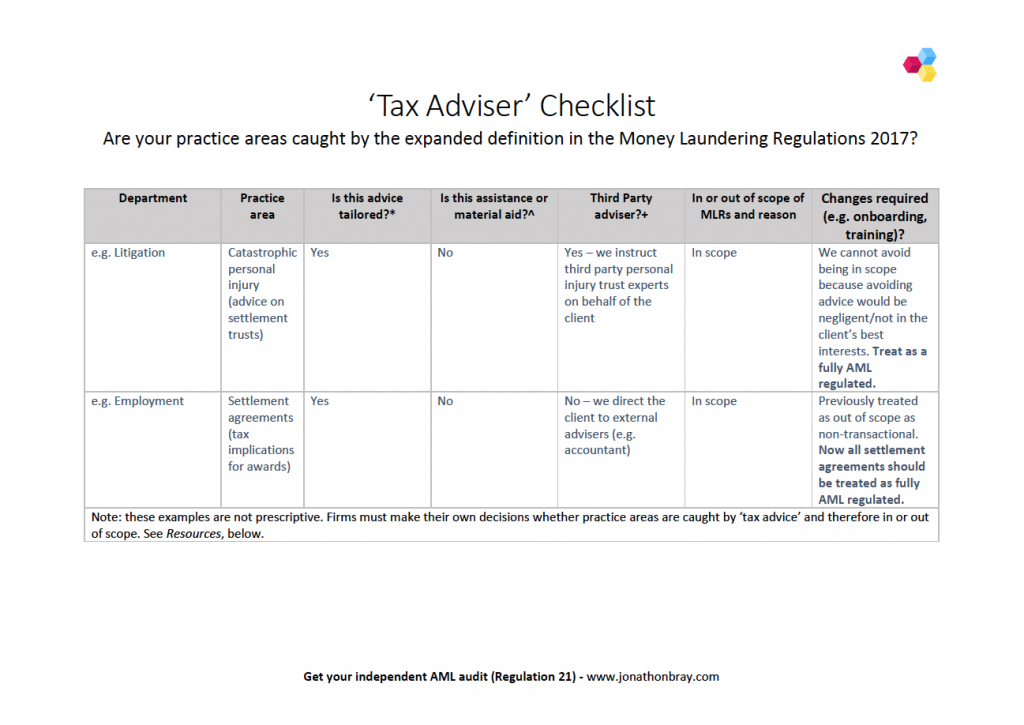

As we previously highlighted (see When is tax advice not tax advice? The implications for solicitors are no joke), it is critically important to determine whether the expanded definition of ‘tax adviser’ in the Money Laundering Regulations is an issue for your firm.

The definition of ‘tax adviser’ has been significantly expanded. This is important for all UK law firms.

See the SRA ‘tax adviser’ guidance for more information.

What do we need to do?

You will need to establish whether any practice areas are brought within scope of the Money Laundering Regulations.

Will writing, personal injury, settlement agreements, pensions – these are all areas of law which could be impacted.

Some firms will have to amend their compliance processes. Others will need to register with the SRA for anti-money laundering authorisation.

At the very least, all law firms have to go through the SRA ‘tax adviser’ thought process.

How do we check our status?

Using this checklist as a starting point, you can demonstrate to the SRA that you have completed the required analysis. And, more importantly, can justify your decisions.

The regulators proactively spot-check AML compliance. Firms that fail to assess their SRA ‘tax adviser’ status could be criticised.

You should also check whether your law firm is properly authorised for AML-regulated work. You may need to make new SRA notifications.

{kind=link}