Overcoming the challenges associated with economic instability looks set to trouble individuals and businesses alike in 2023. Increased wage demands look certain to add to the rising cost of doing business, both fuelled by rising inflation.

The impact of this situation means the Bank of England at their latest raised interest rates on Thursday 15thDecember 2022 to 3.5%, a rise of 0.5% percentage points.

Rising interest rates will be an unwelcome thought for many mortgage holders.

However, for legal practices that hold client monies, rising interest rates should be welcome news.

Your finance function could possibly generate more income in 1 hour than the average fee earner could in 1 year

Sound ridiculous? It’s not. According to the LMS Financial Benchmarking Survey 2022, written by Hazelwoods Accountants, the average fee earner bills £134k per annum with a breakeven point of £121k.

- That means the average fee earner contributes a ‘super profit’ of just over £13k for an entire year’s work

- In contrast, a deposit balance of £5m could generate around £130k per year

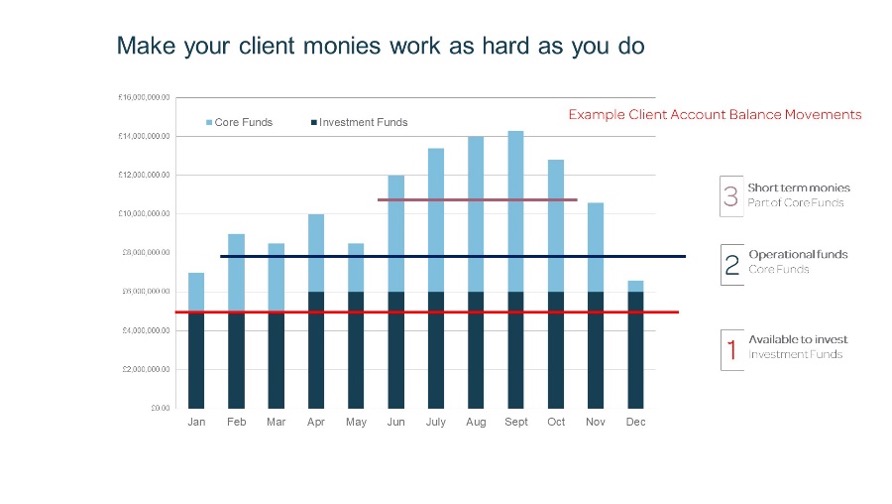

It’s no surprise then that firms are beginning to think hard about their approach toward managing client monies.

The finance function could complete the application forms in under 1 hour and benefit from increased interest income and mitigate some of the risks dealing with a single banking provider

That’s where finance brokers come in, says Paul McCluskey of Gemstone Legal.

“Good brokers can help firms generate maximum income from client funds. We work with banking providers to offer firms the best rates available, without disrupting those important primary banking relationships.

“The primary objective of a law firm is not to maximise revenue from client monies, but as a Partner or Director you can’t ignore an opportunity to generate significant untapped income, often with little effort. There’s even an argument to say that failing to explore the options could put you in breach of your duties to the business.”

What about SRA rules on paying interest to clients? The Accounts Rules say that firms have to ‘account to clients or third parties for a fair sum of interest on any client money held…on their behalf’ (Rule 7.1).

But that does not mean all interest earned on the firm’s client account has to be passed on to clients. Fundamentally, interest earned on a firm’s client account belongs to the firm. It is then up to the firm to decide what is a ‘fair’ amount to pay out, if anything. The main obligation is to have a fair payment of interest policy and stick to it. See our recent post ‘What is a fair amount of interest to pay on client money’ for more information.

With the rising costs of doing business, an uncertain economic outlook and the difficulty of recruiting fee earners to help generate income, law firm leaders must explore opportunities to protect profit levels.

The free ‘Client Money Interest Scorecard’ is the first step to creating a sustainable strategy which will deliver valuable recurring income for your law firm.

Not only could your law firm receive higher interest, but from a risk management point of view you could also benefit by having a contingent banking partner should your primary bankers experience a system failure. It does happen!

Are you ready to earn more interest on your client monies?

Access the free scorecard here.

You will be presented with 12 multiple choice questions which:

- Only takes only 2 minutes to complete

- Helps to uncover how your firm could generate additional income.

- No need to provide any sensitive financial information.

{kind=link}